Farmland

56.7%

56.7%

The market is increasingly recognising nature as critical national infrastructure. Chrysalis focuses on under utilised land with high regenerative headroom. Lower entry cost creates space for measurable improvement and stronger long-term value creation.

Natural and social capital offers inflation protection, diversification and the potential for strong, stable returns. It is becoming a strategic allocation for institutional investors seeking long term resilience and impact, alongside risk adjusted returns from off take agreements and stacked revenue streams.

Many market participants focus on a single outcome, such as Biodiversity Net Gain or carbon.

Chrysalis assesses each site for its optimal mix of biodiversity, carbon, water resilience, social value and energy potential.

By designing for multiple benefits from the outset, we create diversified return pathways and more resilient land strategies.

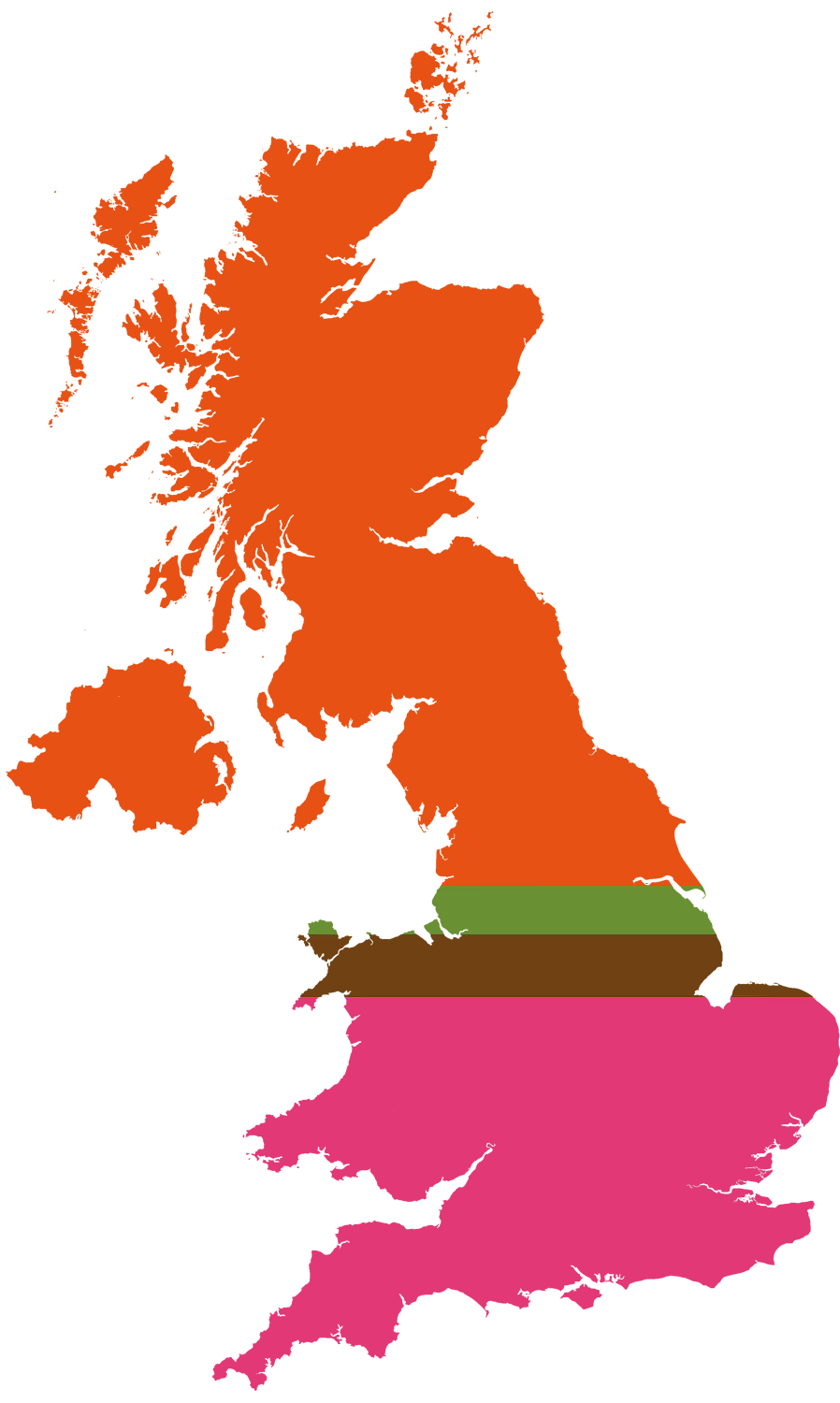

The way land is used across the UK reveals the scale of opportunity that exists. It highlights the wide range of access routes, and the significant potential to bring forward sites through both the open market and established landowner relationships.

The UK regulatory environment continues to strengthen, with Biodiversity Net Gain requirements and wider net zero commitments reshaping land economics.

At the same time, investors and corporates are beginning to recognise nature-related risk within supply chains and operations.

As awareness and disclosure increase, demand for verified biodiversity, carbon and water outcomes is expected to grow.

Returns can be generated through biodiversity units, carbon benefits, flood mitigation outcomes and other emerging natural capital services.

The model is grounded in measurable metrics and conservative assumptions, supporting credibility with institutional capital.

Alongside diversified revenue streams, underlying land ownership provides residual asset value and downside protection.